WLFI: Collateral Loop Breakdown

Table of Contents

Recent activity on Dolomite shows a sharp increase in borrowing tied to World Liberty Finance.

Over the past few days, this team, which already held open positions on the protocol, expanded its exposure materially, pushing WLFI collateral utilization close to its limit and driving a steep change in stablecoin borrowing.

Dolomite, an EVM lending protocol founded by Corey Caplan, who also serves as CTO of World Liberty Fi, enabled borrowing against WLFI with a liquidation threshold set at 66% of collateral value.

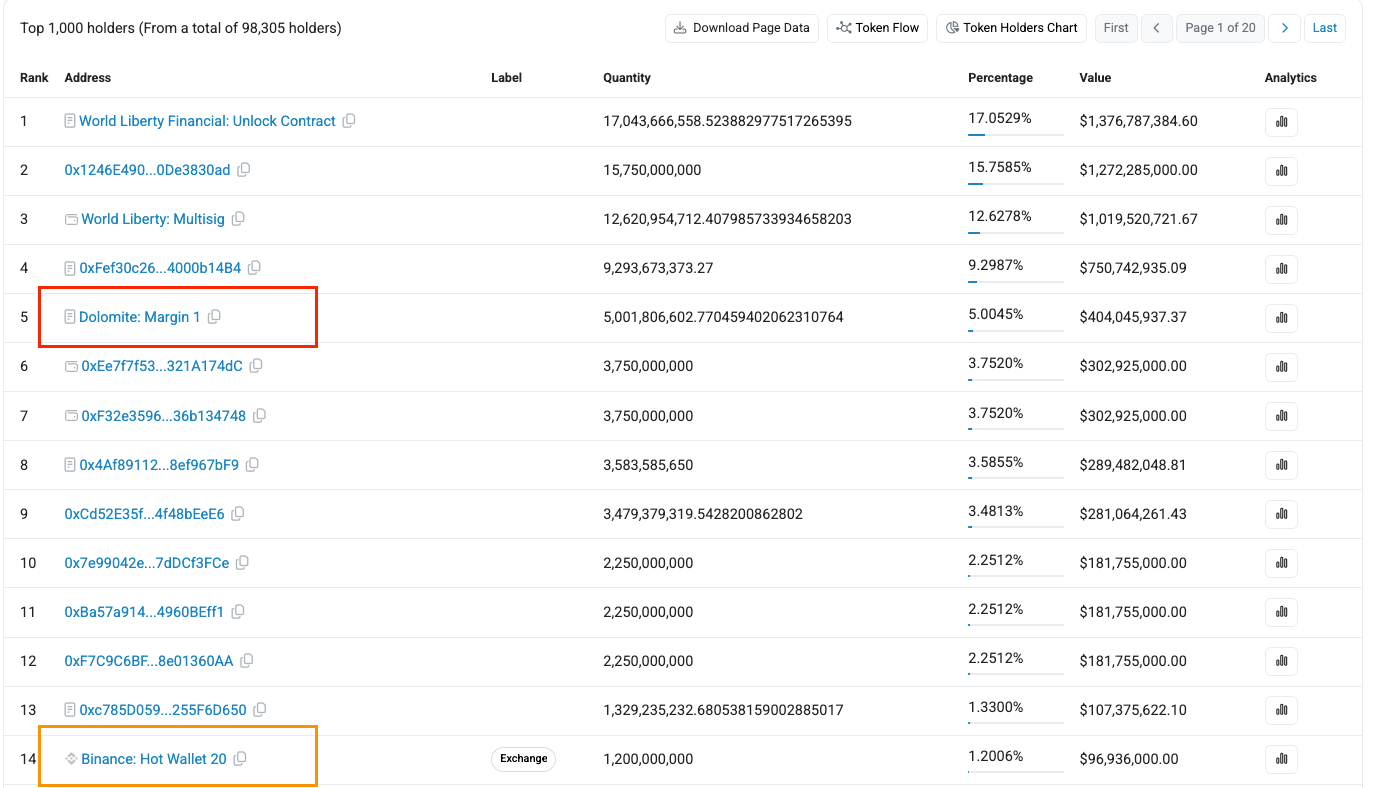

Current collateral cap for WLFI stands at 5.1B tokens and is now almost fully utilized by the World Liberty Finance team across two primary addresses. A wallet corresponding to the team’s multisig (0x5be9…), and another (0x44a6…) a secondary multisig.

Position Structure

Much of the discussion around these positions misses the underlying structure:

- Wallet 0x44a6 borrowed approximately $40.7M in stables, primarily USD1, against 3B WLFI, valued at ~$242M at the time of writing. This implies a liquidation threshold corresponding to an approximate 75% decline in WLFI price.

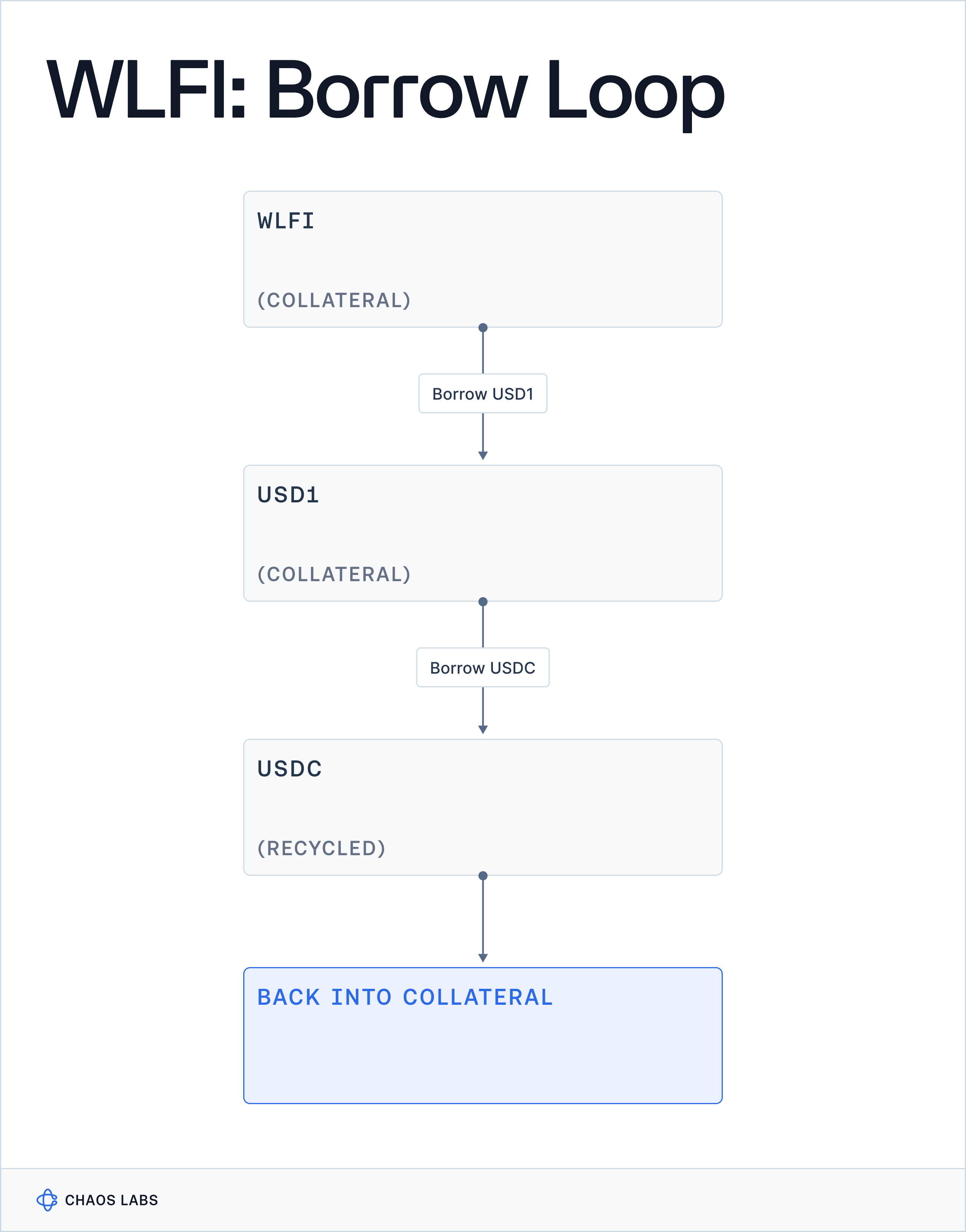

- Wallet 0x5be9 accounts for the majority of the borrowing and follows a more complex structure. It holds two positions: $111M in USD1 borrowed against a mix of WLFI ($161M) and USDC ($98M), and $89M in USDC borrowed against $110M in USD1. In effect, USD1 borrowed in the first position is used as collateral to borrow USDC in the second, which is then cycled back as collateral into the first position.

The rationale behind this structure has not been disclosed. Based on the current configuration, WLFI would need to decline by approximately 75% before reaching liquidation levels, assuming USD1 maintains its peg.

A few interpretations have been suggested.

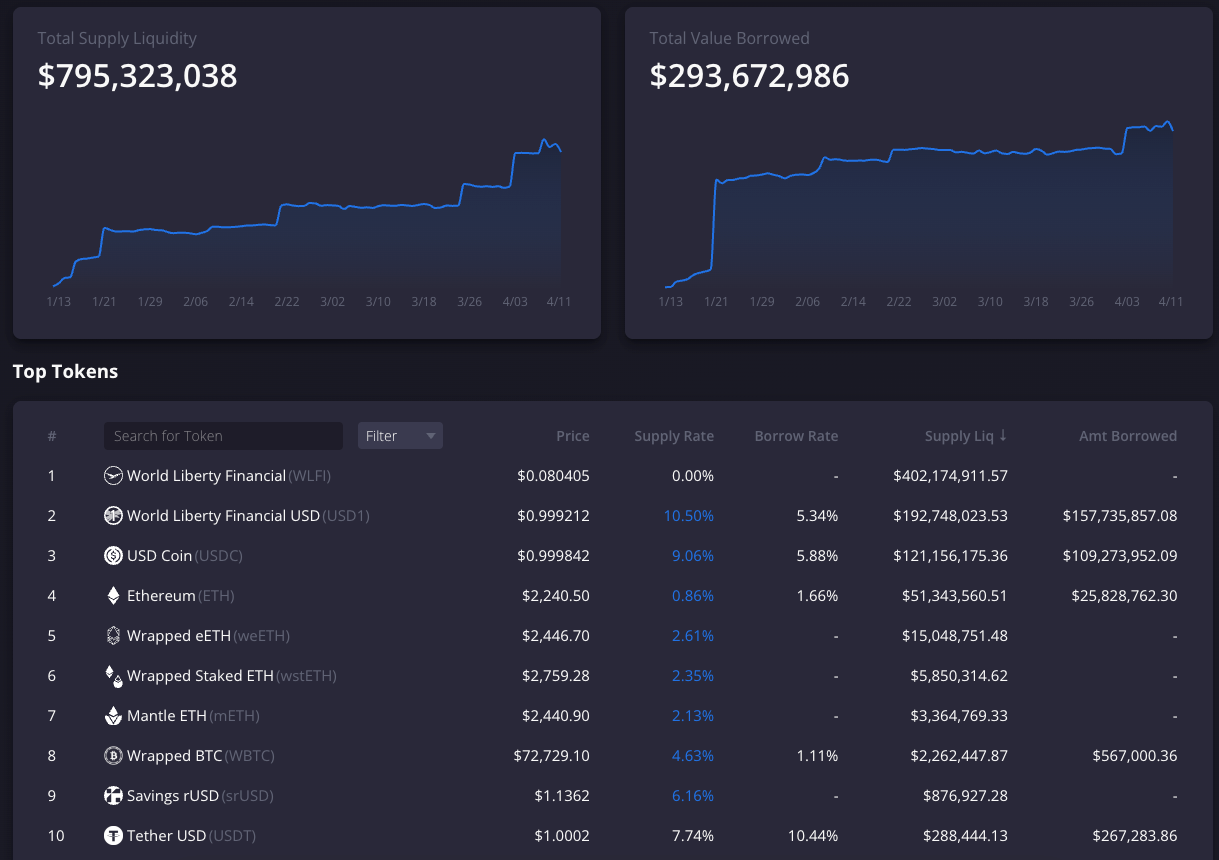

One interpretation is that this activity increased utilization and rates on Dolomite for USD1 and USDC, incentivizing usage. USD1 utilization rose to 83.4%, with supply rates at 10.64% when including WLFI rewards via Merkl (the Merkl campaign ends in three days). USDC utilization reached 90.19%, with supply rates at 9.07%. Borrow rates for both assets moved into the 5% range, pushing most non-WLFI-related looped strategies into negative returns.

Merkl rewards are calculated on net lending, which limits the extent to which this structure generates rewards on recycled positions.

Other interpretations include liquidity needs, a preference to borrow rather than sell or burn USD1, positioning ahead of investor unlocks, or preparation for exits under current risk parameters.

Market Implications

While mid-to-high LTV lending against governance tokens is not unprecedented, Dolomite itself offers comparable parameters for assets such as CRV, the structure here warrants closer attention.

- First, the quantity of WLFI used as collateral exceeds four times the total tokens available on the largest exchange venue, Binance.

- Second, while WLFI’s headline market capitalization exceeds that of assets like AAVE and CRV, its effective circulating supply and trading liquidity across centralized and decentralized venues is materially lower.

- Third, only 20% of WLFI has been unlocked to investors, with the remaining 80% pending a governance decision expected in mid-April. Most of the supply is therefore not participating in price discovery. Investors, currently at approximately 1.88x ROI, may choose to realize gains once tokens unlock.

The situation is likely to evolve further once the unlock proposal is formally introduced. Following public scrutiny, the team repaid approximately $10M in USD1 and indicated a willingness to provide additional collateral if required.

The multisig at 0x5be9 currently holds an additional $1.02B in WLFI, which could be deployed as collateral if supply caps increase. It also holds approximately $27M in USD1 that could be used for further repayments.

World Liberty Finance accounts for 82.7% of total TVL supplied to Dolomite and 85.3% of total assets borrowed. In practice, activity is highly concentrated: collateral is supplied by the same entity driving borrowing, and liquidity is largely recycled across the same set of addresses.

The New Source of Edge in Financial AI

In finance, where outcomes depend on precision, timing, and execution, generic intelligence does not sustain an edge. As reasoning converges and access expands, competition shifts toward the application of intelligence.

The Market Crypto Never Built

Crypto never built the infrastructure layer that makes financial systems safe enough to deserve the trust people place in them. Without a forcing function, the industry spends on protection as if it's optional while losing billions to exploits it could have prevented.

Risk Less.

Know More.

Get updates on our research, product, and launch.