Aave v4: A Design Framework for Pooled and Isolated Bluechip Collateral Markets

Table of Contents

Overview

The objective of this analysis is to establish a structured foundation for governance discussions on how bluechip collateral should be configured in Aave v4, and to clearly articulate the trade-offs, benefits, and risk implications associated with each design approach.

By combining hubs, spokes, and allocation mechanisms Aave v4 lets us approach a fresh design space, where we aim to both maximize capital efficiency and strictly reduce liquidity and rehypothecation risk for users or entities with specific requirements. This is achieved through the use of fully isolated markets, where collateral is never rehypothecated, and as such, liquidity risk is fully mitigated in the context of both withdrawals and liquidations.

This analysis examines how these architectural choices can be applied to bluechip collateral.

In this context, bluechip collateral specifically refers to WETH, WBTC, and cbBTC. We outline multiple potential bluechip market designs ranging from the traditional pooled model to fully isolated collateral environments. Each design serves a different borrower and lender risk profile and presents a distinct combination of borrowing power, liquidity considerations, counterparty exposure and risk parameter flexibility.

What this analysis is NOT intended to cover

This report does not evaluate or make recommendations regarding which assets should be listed on Aave v4. It also does not provide guidance on risk parameterization for wide range of assets. Finally, this analysis does not examine how hubs and spokes should be configured for non-bluechip collateral. The scope is purposefully limited to the design space for WETH, WBTC, and cbBTC within Aave v4, in order to start a focused technical discussion before extending the framework to a broader set of assets.

Market Designs for Bluechip Collateral

This section presents the full range of market design choices available for bluechip collateral. We outline each configuration individually and describe its native implementation under the Aave v4 infrastructure. Furthermore, we cover each configuration’s strengths and weaknesses, focusing on borrowing power, liquidity considerations, counterparty exposure, and parameter flexibility. After examining the designs one by one, we consolidate their features into a comparative analysis table to provide a clear assessment. The section concludes with our recommended structure for bluechip assets, which aims to serve a broad spectrum of borrowers and lenders with different risk preferences while maintaining a unified liquidity environment and avoiding unnecessary fragmentation.

1. Pooled Core Spoke

The pooled Core Spoke represents the most general and widely accessible configuration within the hub-and-spoke framework. In this building block configuration, a broad set of collateral assets is combined into a single pooled environment that closely mirrors the structure of the current Aave v3 Core market. The shared collateral base enables cross collateralization across many asset types, which in turn necessitates the use of the most conservative risk parameters within the v4 design space.

In this model, deposited assets are rehypothecated to generate yield based on borrower demand. Bluechip assets, such as WETH, WBTC, and cbBTC are listed alongside other collateral assets, providing a familiar user experience and a risk profile that is consistent with the pooled model used today. This structure also benefits from direct access to the protocol's deepest stablecoin reserves, which support interest rate stability and ensure efficient borrowing conditions for users.

2. Bluechip Stablecoin Spoke with Cross Margin

The bluechip stablecoin spoke is a dedicated configuration that allows WETH, WBTC, and cbBTC to be used as collateral to borrow stablecoins while retaining cross-collateral functionality within the spoke. This structure creates a focused environment for pristine assets.

The spoke continues to benefit from the deep stablecoin liquidity of the core hub, which supports rate stability and efficient borrowing conditions. Conceptually, it resembles the E Mode configuration in Aave v3, but with additional precision. As covered in our analysis Aave v4: New Features and Risk Parameter Analysis, v4 introduces several spoke-level parameters regarding how liquidation should work, including targetHealthFactor, liquidationBonusFactor, and healthFactorForMaxBonus. These can be tuned specifically for bluechip assets to offer a more protective liquidation environment for borrowers, reflecting their lower risk profile.

Collateral within this spoke remains rehypothecated, enabling borrowers to earn a yield on their collateral. While bluechip assets can receive more favourable parameterization than in the general pooled environment, cross-collateralization remains an important constraint. The volatility or utilization spike of one asset within the spoke affects the risk profile of the others during stress scenarios, which limits the aggressiveness of the parameter settings. This interdependence prevents collateral assets from reaching the more competitive risk settings achievable in segmented configurations, which we discuss in the following section.

3. Bluechip Stablecoin Spokes

Bluechip stablecoin spokes represent a more segmented configuration in which each pristine collateral asset is placed into its own dedicated spoke. Unlike the cross-margin design discussed earlier, this structure does not allow WETH, WBTC, and cbBTC to serve as collateral for one another. Each asset operates within an independent environment that maintains a clear separation of risk between collateral types.

This configuration enables spoke-level liquidation parameters to be tailored to the specific characteristics of each individual blue-chip asset. Parameters can therefore be optimized in a more focused manner than in a cross-collateralized structure, where inter-asset volatility places limits on parameter flexibility.

Collateral within these spokes continues to be rehypothecated, allowing borrowers to earn yield on their collateral based on utilization. Borrowers retain access to the deep stablecoin liquidity of the core hub, and the design does not introduce any liquidity fragmentation.

The removal of cross-collateralization allows these spokes to support higher borrowing power compared to a shared blue-chip spoke. By separating the collateral assets from one another, the design reduces the transmission of correlated risk and enables more competitive parameterization.

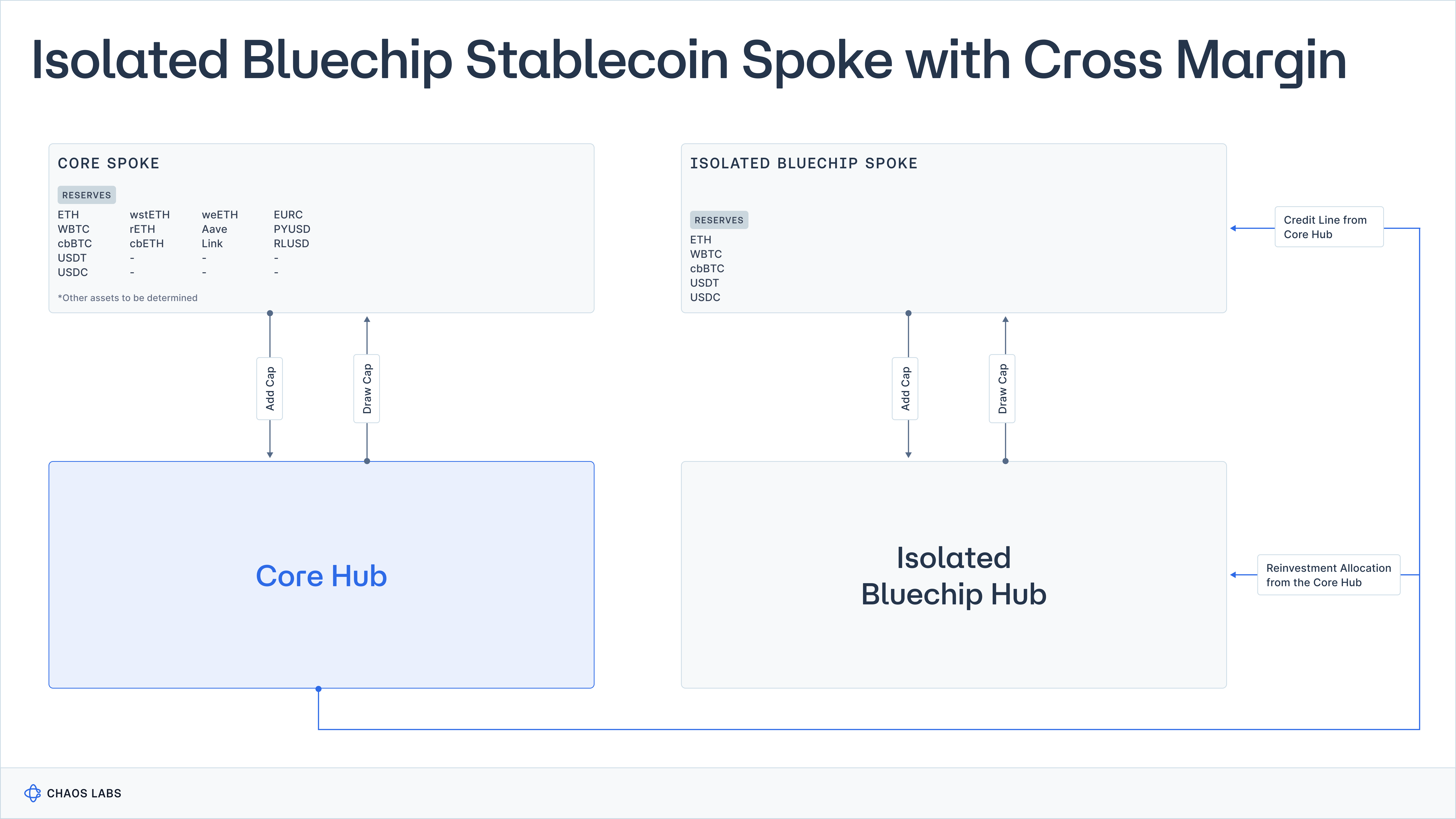

4. Isolated Bluechip Stablecoin Spoke with Cross Margin

The isolated setups introduce a separate hub-and-spoke structure dedicated solely to bluechip collateral, while still allowing cross-collateralization between WETH, WBTC, and cbBTC. In this configuration, bluechip assets are not borrowable, and their primary function within the hub is to serve as collateral for stablecoin borrowing.

A defining feature of this design is the removal of rehypothecation. Collateral is never lent out within the isolated hub, which ensures that borrowers retain full and immediate access to their collateral at all times. As a result, borrowers are not exposed to liquidity risk during periods of elevated utilization. Furthermore, borrowers do not underwrite the obligations of other borrowers, as the setup prevents collateral from being serviced for separate borrowing positions as debt. This eliminates solvency and default risk stemming from the behavior or risk profile of other borrowers.

The absence of collateral utilization also strengthens the protocol’s risk posture. Because the collateral is never deployed into lending activity, the hub maintains complete liquidity for liquidations under stress scenarios. This removes the risk of liquidations being halted due to limited available liquidity, ensuring that the protocol can always execute liquidations when required. As a result, the structure supports more competitive risk parameters meaningfully, reflecting the reduced systemic risk within a fully isolated environment.

This configuration is particularly well-suited for borrowers who do not want their collateral to be rehypothecated and who value guaranteed availability of their deposited assets at all times. It is also an attractive environment for stablecoin suppliers who prefer to underwrite only pristine collateral and avoid exposure to a broader mix of assets.

The separate hub introduces liquidity fragmentation, as it does not have direct access to the deep, stablecoin liquidity of the Core Hub. This can be addressed by establishing credit lines from the Core Hub and/or through the reinvestment controller, which allows idle stable liquidity from the Core to be allocated to the Isolated Hub when needed. Both approaches come with trade-offs and operational considerations that require separate and detailed analysis beyond the scope of this work.

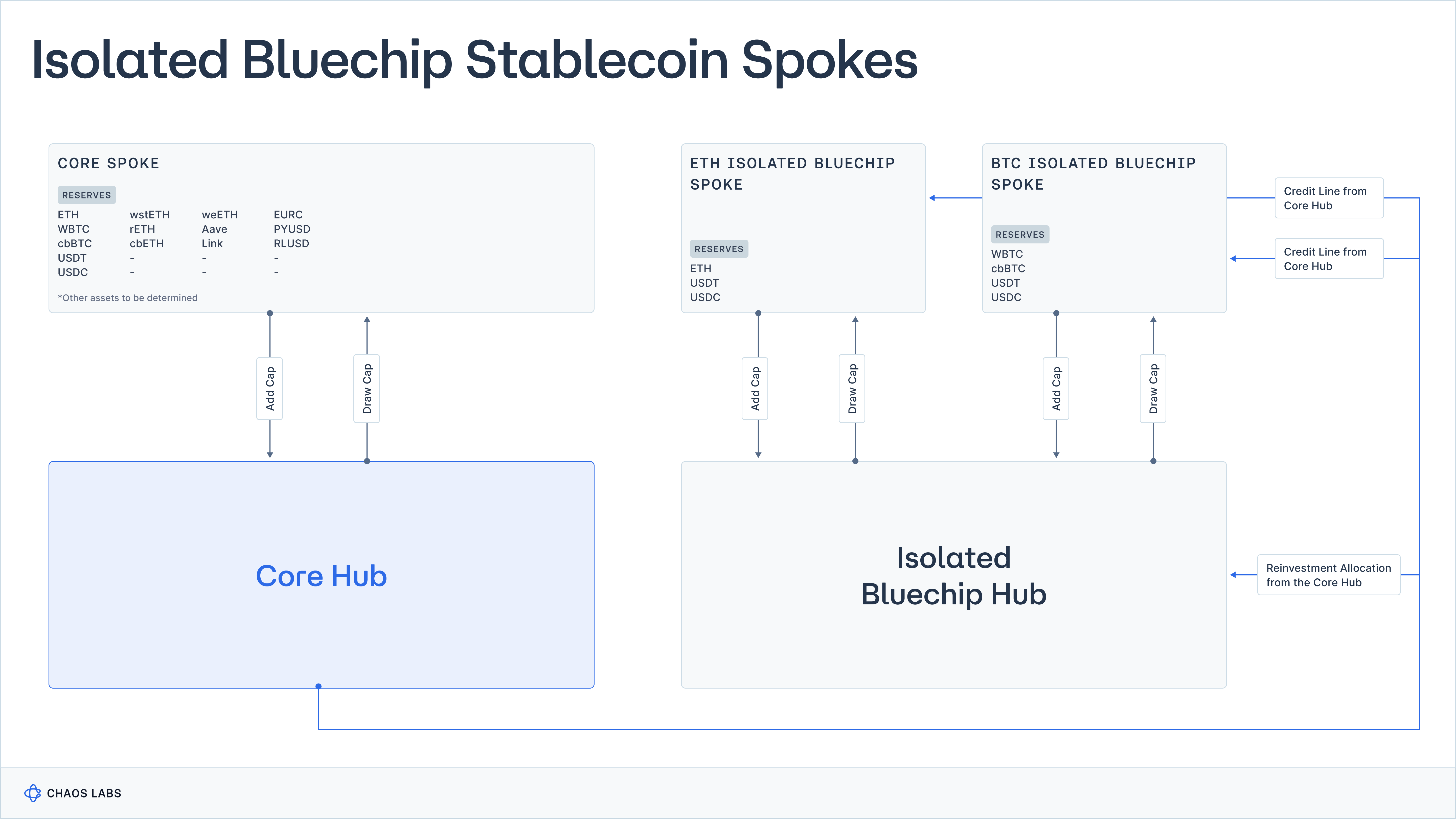

5. Isolated Bluechip Stablecoin Spokes

The isolated bluechip stablecoin spokes represent a configuration that closely resembles the cross margin version described in the previous section, with one key distinction. Instead of placing WETH, WBTC, and cbBTC together within a single isolated spoke, this design creates a separate spoke for each bluechip asset within the Isolated Hub. Each collateral type therefore operates fully independently while still benefiting from the isolated environment where no rehypothecation occurs.

This structure offers additional granularity in how spoke level liquidation parameters can be calibrated. However, the incremental benefit of this additional separation is relatively limited. Since collateral is never utilized in the isolated hub and full liquidity for liquidations is always available. As a result, while this design increases parameter flexibility, the practical improvement over a unified isolated bluechip spoke is marginal.

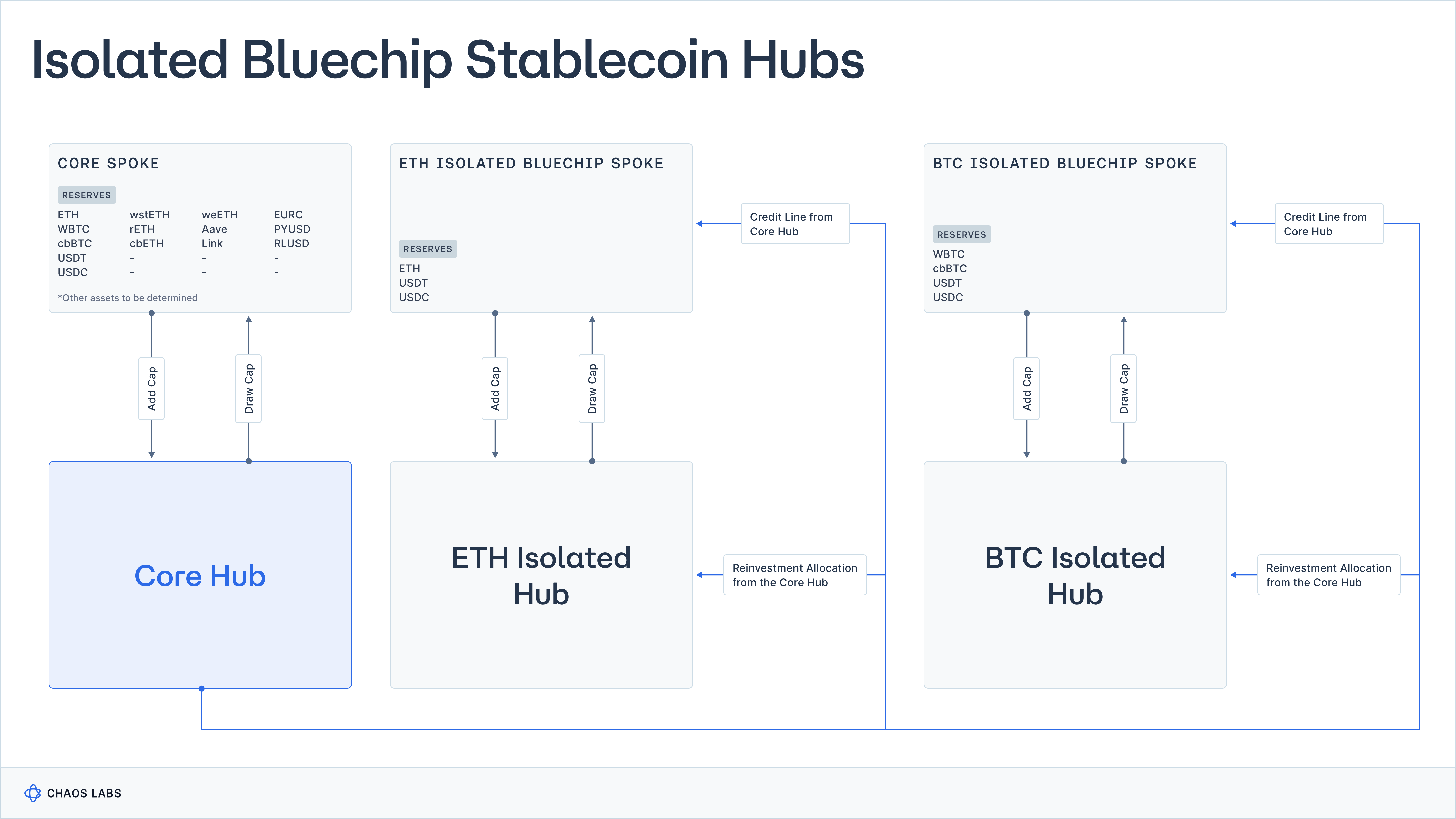

6. Isolated Bluechip Stablecoin Hubs

The isolated bluechip stablecoin hubs represent the most segmented configuration within the design space. In this structure, each collateral asset, such as WETH and WBTC or cbBTC, is placed not only into its own spoke but also into its own dedicated hub. This results in completely independent markets for each bluechip asset, where collateral is never rehypothecated, and borrowers can only borrow stablecoins against a single type of pristine collateral.

While this approach preserves all the advantages of isolation, it materially increases liquidity fragmentation. Each hub must maintain its own supply of stable liquidity, and the absence of shared liquidity pools reduces the depth available to borrowers. Managing liquidity across multiple isolated hubs also requires more complex routing or credit line frameworks.

The incremental value of this design is limited. Its primary benefit is that it caters to stablecoin suppliers who may prefer to underwrite debt exclusively against a specific pristine collateral. However, onchain evidence from other isolated lending protocols suggests that suppliers rarely distinguish between bluechip assets to this degree, which reduces the practical demand for fully separated hubs.

One potential advantage of this configuration is the ability to implement distinct interest rate models for each collateral asset. This may offer some value where collateral-specific dynamics or borrower demand patterns justify bespoke rate shaping. Nevertheless, this benefit must be weighed against the considerable fragmentation and operational overhead introduced by maintaining multiple isolated hubs.

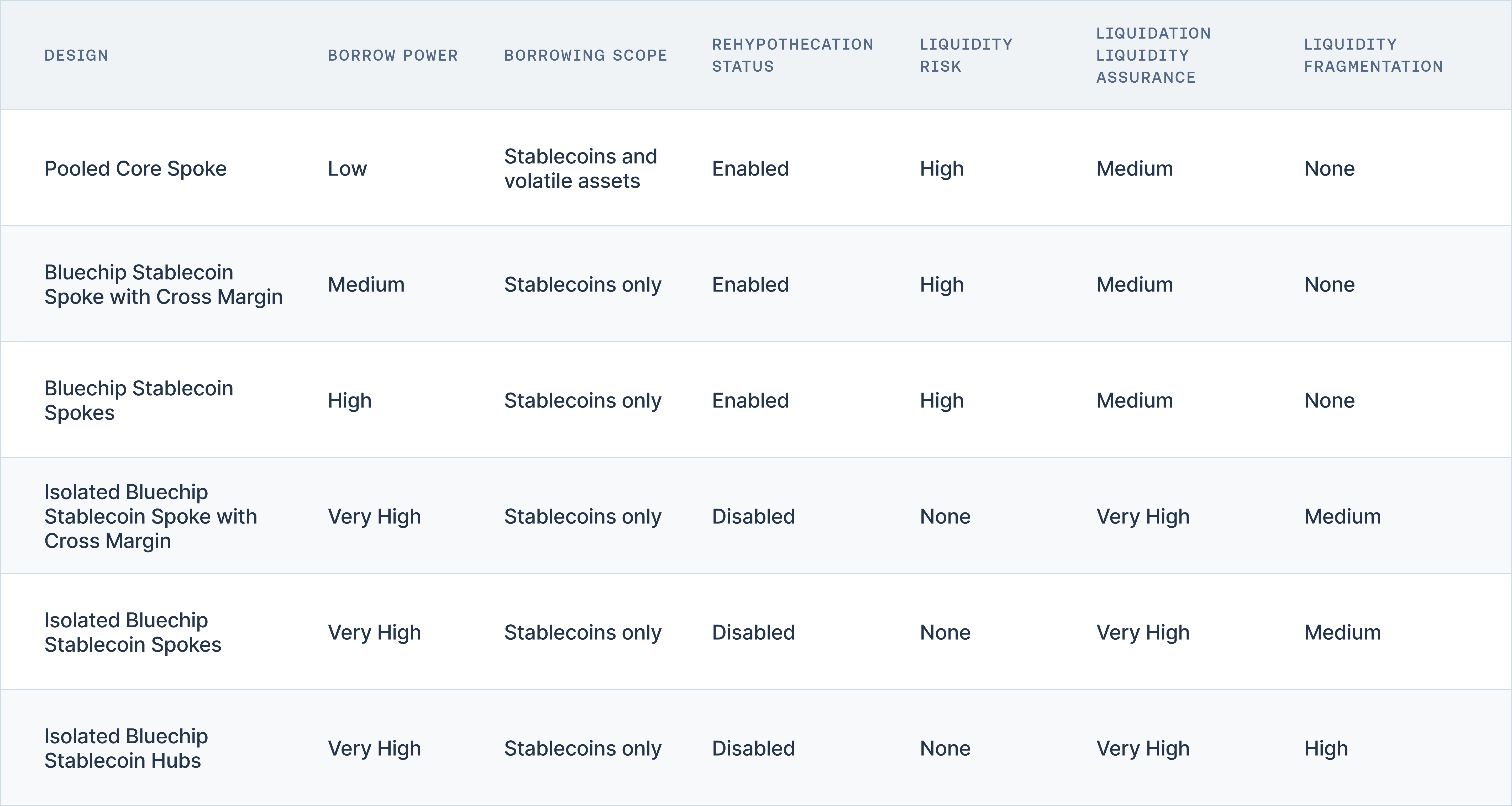

Comparative Analysis of the Designs

The table below summarizes the key trade-offs across the bluechip market designs by comparing borrowing power, borrowing scope, collateral treatment, liquidity characteristics, and parameter flexibility. Moving from the pooled Core Spoke toward increasingly isolated configurations, borrowing power and parameter flexibility increase as rehypothecation and cross-asset dependencies are removed. This progression comes at the cost of reduced composability and, in some cases, increased liquidity fragmentation.

Taken together, the table illustrates that no single design dominates across all dimensions. Instead, the optimal configuration emerges from combining multiple designs to balance capital efficiency, risk isolation, and liquidity fragmentation, allowing Aave to serve diverse borrower and supplier preferences within a coherent market structure.

All values in the table are relative and intended to compare designs against each other rather than define absolute thresholds.

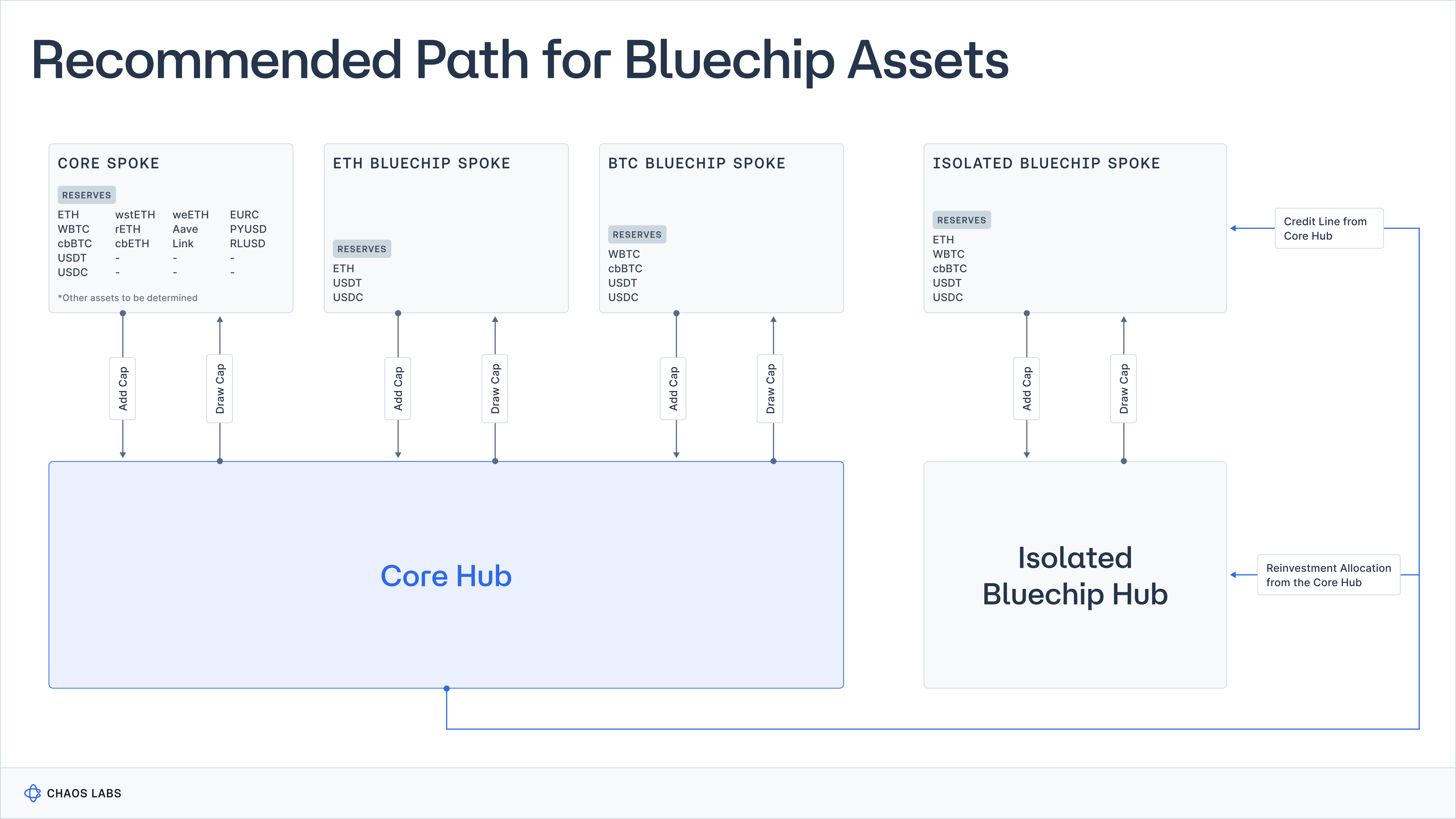

Recommended Path for Bluechip Assets

The objective of the recommended configuration is to serve a wide range of borrowers and stablecoin suppliers with varying risk appetites, while avoiding unnecessary liquidity fragmentation and preserving the efficiency of the broader Aave v4 market. Rather than selecting a single design, we propose a layered structure that leverages multiple configurations in parallel, each serving a distinct user profile.

First, we recommend maintaining a pooled Core Spoke within the Core Hub, configured with conservative parameters. This spoke serves as the foundational building block of the market and closely mirrors the user experience and risk profile of the Aave v3 Core market. It enables broad cross-collateralization, supports borrowing of both stablecoins and volatile assets, and provides direct access to the deepest liquidity pools in the protocol.

Second, within the Core Hub, we recommend introducing segmented Bluechip Stablecoin Spokes for each pristine collateral asset. Given the high utilization and systemic importance of assets such as WETH, separating bluechip collateral into dedicated spokes allows for improved parameterization. These spokes preserve access to Core Hub liquidity, avoid fragmentation, and enable higher borrowing power than the pooled Core Spoke.

Third, we recommend deploying an Isolated Bluechip Hub with a unified Bluechip Spoke that supports cross collateralization between WETH, WBTC, and cbBTC. In this isolated environment, collateral is not rehypothecated because bluechip assets are not borrowable. This configuration offers an alternative borrowing path for users who prioritize collateral availability, minimize liquidity risk, and avoid underwriting other borrowers. The isolated hub can be bootstrapped through reinvestment allocations from the Core Hub and supported by credit lines that allow it to tap into core stablecoin liquidity when required.

Taken together, this structure offers borrowers three distinct risk and capital efficiency profiles.

By using the pooled Core Spoke, borrowers access a fully pooled borrowing experience similar to Aave v3, with the ability to borrow both stable and volatile assets against a broad set of collateral in conjunction with bluechip collateral, but with lower borrowing power.

By using the Bluechip Spokes within the Core Hub, borrowers give up the ability to borrow volatile assets and to use cross collateralization, but achieve higher borrowing power than in the pooled Core Spoke, without sacrificing access to the deep and stable liquidity of the Core Hub.

By choosing the Isolated Bluechip Spoke, borrowers accept the trade-off of foregoing collateral yield and direct access to Core Hub stablecoin liquidity in exchange for maximum borrowing power, no liquidity risk, no rehypothecation, and no exposure to the solvency of other borrowers.

This layered approach allows Aave v4 to accommodate materially different borrower and supplier preferences without excessive liquidity fragmentation or forcing a single risk profile onto all users.

Additional details: https://governance.aave.com/t/aave-v4-a-design-framework-for-pooled-and-isolated-bluechip-collateral-markets/23839#p-60984-h-4-isolated-bluechip-stablecoin-spoke-with-cross-margin-6

AI as Operational Infra for Risk-Aware Execution

We propose a shift towards a system (or copilot) that maintains continuous situational awareness and translates live market state into decision-ready options within user-defined constraints.

(Part 2) The Limits of Web Search For Financial AI

In most software systems, performance is a user-experience concern. In finance, data freshness defines validity.

Risk Less.

Know More.

Get updates on our research, product, and launch.