mF-ONE: Private Credit, Public Liquidity

DeFi’s latest panic traces back to an unlikely source: a bankrupt auto-parts supplier based out of Cleveland.

High-yield credit wrapped for composability, pledged at aggressive LTV ratios, and funded by concentrated lenders has exposed the limits of the RWA model.

The offchain exposure

When First Brands Group filed for Chapter 11 in September 2025, few outside distressed-credit desks paid much attention. The company looked like another overlevered industrial borrower squeezed by tighter financing.

By January, the case had escalated.

Federal prosecutors in Manhattan charged former executives, alleging a multibillion-dollar fraud built on fake or inflated invoices and collateral pledged more than once. Court filings pointed to roughly $2B in disputed factoring arrangements and off-balance-sheet financing tied to the collapse.

Buried in the creditor list was Fasanara, an asset manager named in the bankruptcy filings with a $26M unsecured supply-chain finance claim tied to the First Brands estate. While this claim did not identify which vehicle held the exposure, it made one thing clear: a Fasanara-linked credit strategy had direct exposure to the First Brands bankruptcy.

The truth was hidden in public

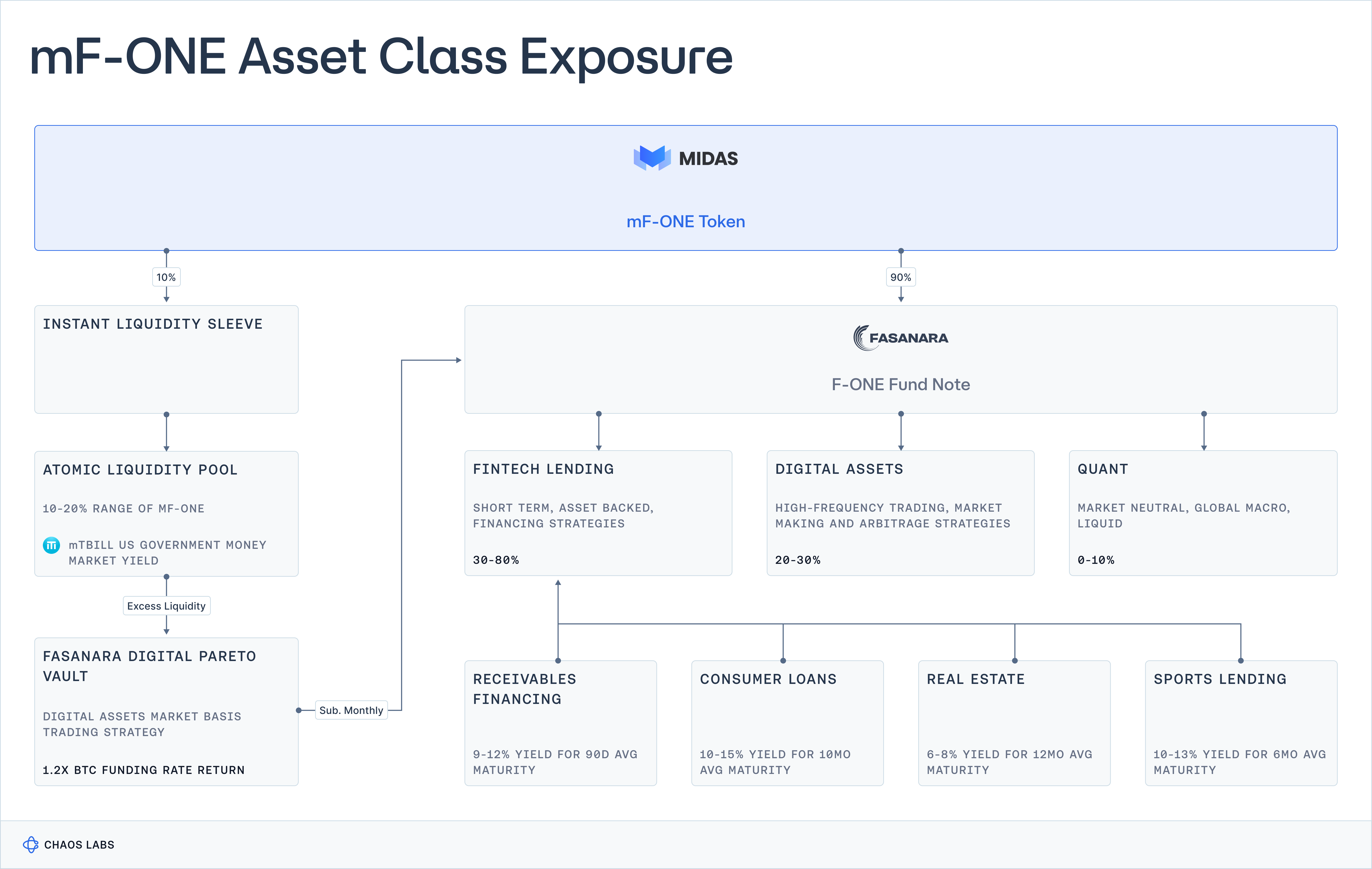

Three months before First Brands filed for bankruptcy, Midas, a tokenization platform focused on RWAs, launched mF-ONE, a product designed to track Fasanara’s F-ONE multi-asset fund and make the strategy composable across DeFi markets.

F-ONE targets sub-15% annual returns through a portfolio weighted primarily toward fintech lending, alongside consumer loans, real estate bridge financing, sports receivables and digital-asset arbitrage. The strategy employs leverage of about 1.3-1.5x. Importantly, mF-ONE embedded additional liquidity layers to its underlying fund exposure, including:

- an instant-liquidity sleeve providing onchain T-bill exposure via mTBILL

- an intermediate liquidity management layer

- core exposure to Fasanara’s F-ONE fund

This design repackaged a levered private-credit strategy into a composable DeFi asset, deployable across onchain markets.

The token was then posted as collateral in the mF-ONE/USDC market on Morpho on Ethereum at an effective LTV of roughly 84.5%, combining a 91.5% market-level parameter with a 7.7% NAV-oracle price discount.

A Timeline of Recent Events

By late 2025, the RWA market was already fragile, following depegs, credit-vault stress and several near failures across the sector.

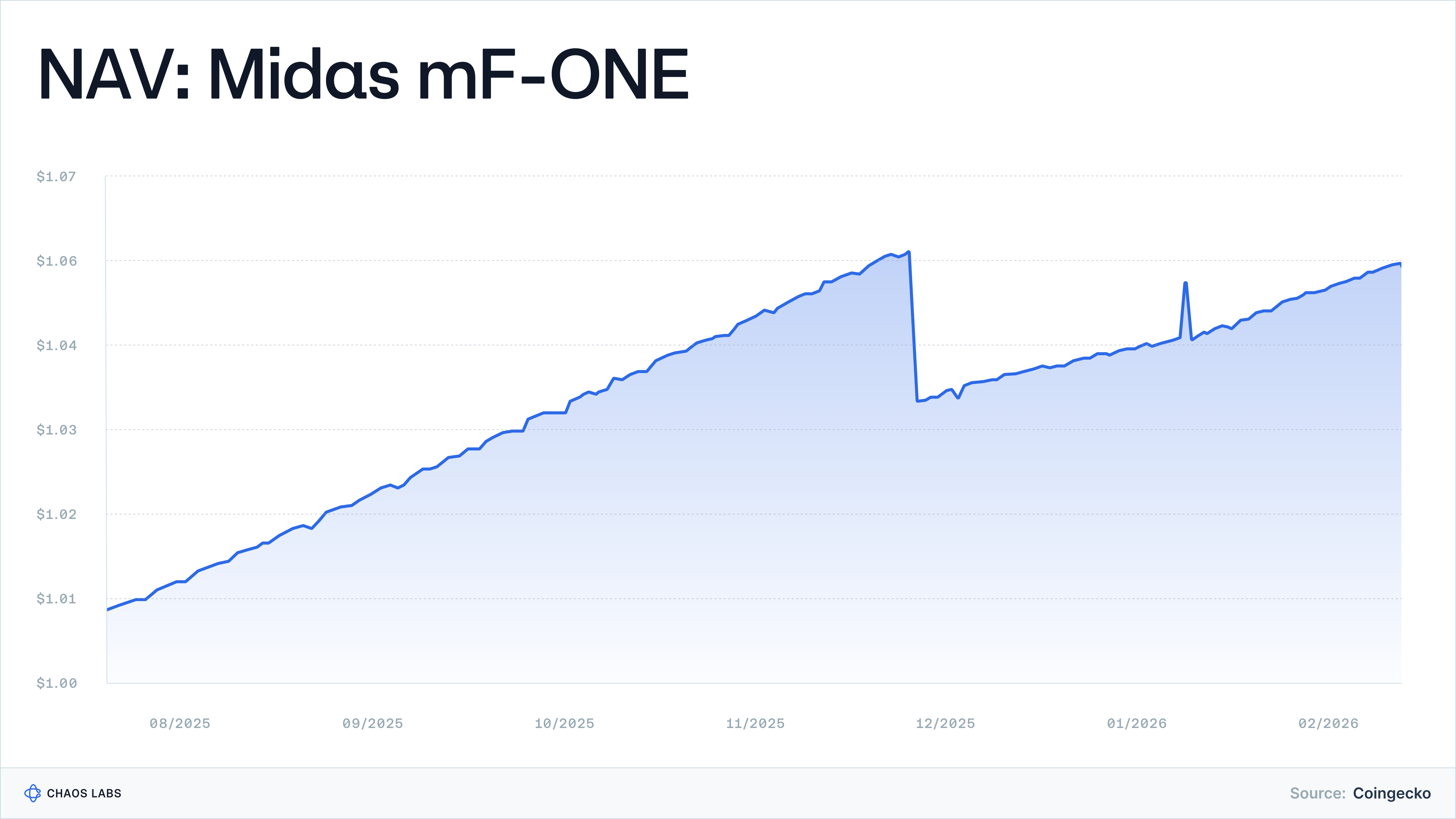

In December 2025, mF-ONE’s NAV declined by about 2% after Fasanara’s fund administrator applied more conservative assumptions to a large default linked to the First Brands bankruptcy. The updated NAV was transmitted onchain via the mF-ONE oracle.

The markdown reflected a realized private-credit impairment. Morpho lenders were not affected. Market risk parameters absorbed the drawdown without generating bad debt.

In this environment, positioning mattered more than headlines, and within a few days, the following conditions aligned:

- Viral posts resurfaced the First Brands and Fasanara link and linked it to mF-ONE

- A large, highly leveraged borrower in the mF-ONE/USDC Morpho market operated near a 1.04 health factor, only a few percentage points from liquidation

- A highly concentrated lender base, with Smokehouse USDC accounting for ~86% of deposits

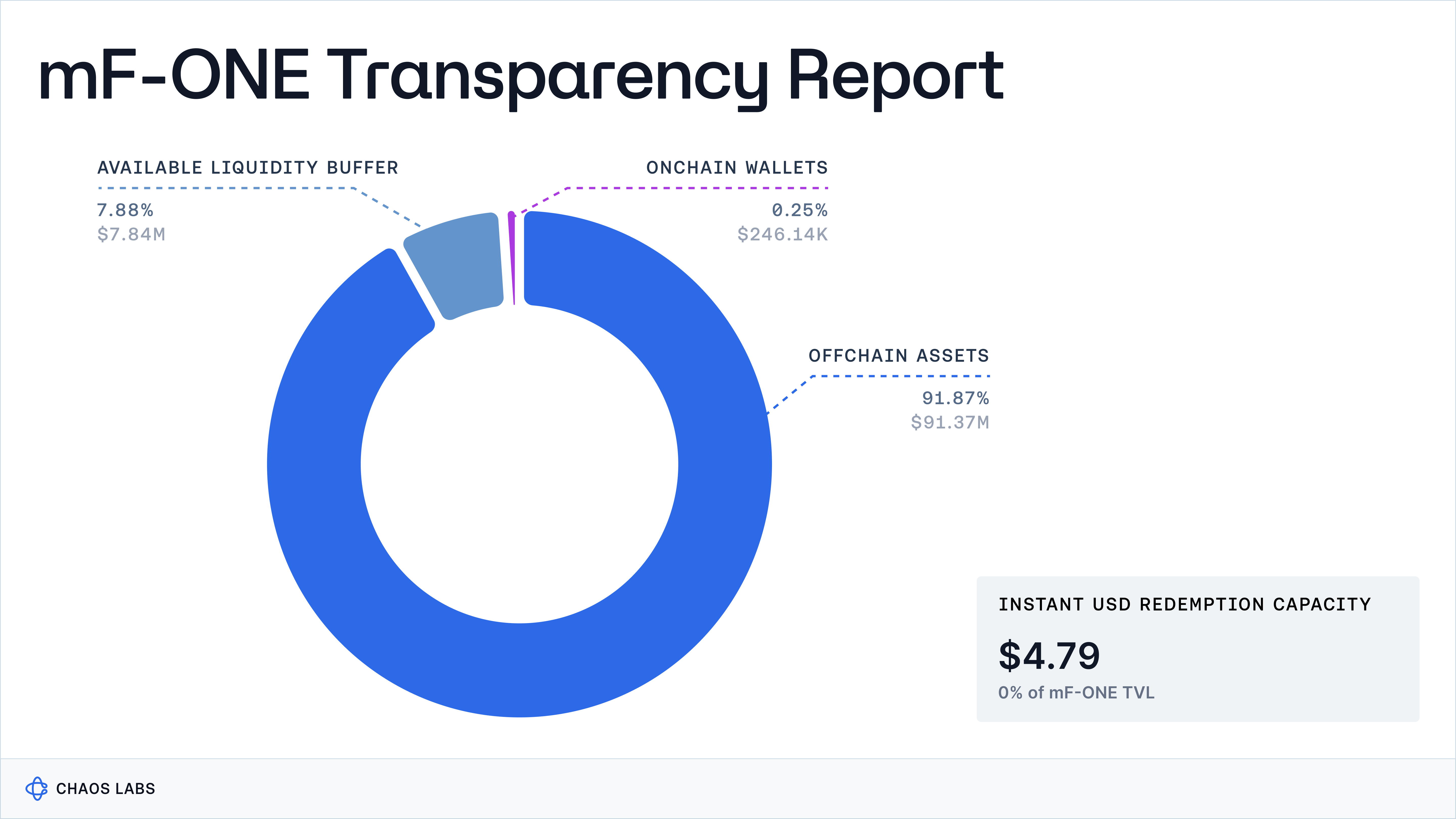

- An apparent delay in mF-ONE burning and supply adjustment, visible in Midas’ daily reports as a mismatch between reported price and collateral beginning Jan 13th 2026

- Utilization spiked to ~97.5%, pushing borrow rates to ~16%, while instant redemption capacity fell toward zero

Taken together, the datapoints resemble patterns seen in previous stress episodes: depleted liquidity, elevated borrowing costs, constrained redemptions and highly leveraged positions near liquidation.

Whether conditions have materially changed since December remains unclear, but public disclosures show no additional impairment at Fasanara beyond the earlier 2% NAV markdown, aside from the criminal charges filed against former First Brands executives.

The renewed stress therefore reflects market structure and positioning rather than confirmed credit deterioration. It also exposes the limits of a model in which leveraged private credit is tokenized and financed at high LTV inside money markets, where liquidity can tighten faster than fundamentals change.

Conclusion: Yield Is Risk

In the push to institutionalize DeFi through RWAs, labels have started to substitute for analysis. “Regulated,” “off-chain,” “FCA-authorised,” “factored receivables,” and “multi-asset credit” are often used as shorthand for “safe” or “cash-like,” even when the term sheets say otherwise.

A fund that targets 15% net per year, uses 1.3–1.5x leverage, and allocates heavily to private credit, consumer loans, real estate bridges, sports receivables, and digital-asset arbitrage is not a stability product. It is a risk product. In traditional finance, that is obvious: double-digit yields sit in the high-yield, private-credit, and special-situations segment of the curve, and participants price them accordingly.

Tokenisation and DeFi composability do not change that. Risk does not disappear simply because it is placed on a blockchain.

The lesson is one we have repeated in recent weeks:

- Off-chain doesn’t mean safe by default. RWAs provide onchain users access to a diverse, sometimes uncorrelated set of yields, but they also introduce legal, operational, and informational complexity that must be priced and monitored.

- Onchain doesn’t mean unsafe by default. A battle-tested CDP relying on ample overcollateralization with BTC and ETH can be safer than many off-chain credit products. There is a reason users pay ~4% for one and up to ~20% for the other.

High yield isn’t just a marketing headline and yield is never risk-free.

When Pricing Becomes Execution: Chaos Oracles are live on Tempo

Tempo, a blockchain incubated by Stripe and Paradigm, has integrated Chaos Price Oracles to power asset valuation across its network.

Yield as a Risk Signal: Part III

If yield is repriced risk, then the critical question becomes: what is the baseline?

Risk Less.

Know More.

Get updates on our research, product, and launch.